EU EV Tariffs ... What Next?

Whack-a-mole.

Last week I wrote:

I’ve probably missed some, but taking into account all of the above, I reckon the standard guess of a default tariff somewhere in the 10-20% range (on top of the existing 10%) is about right. But I wouldn’t be surprised if one or more of the sampled firms is hit with a company-specific tariff that is higher. Let’s go for … a total of 37.5% (10+27.5).

Tune in next week to find out whether I was spectacularly right, in which case I will link back to this post, or spectacularly wrong, in which case we shall never speak of it again.

And the results are in!

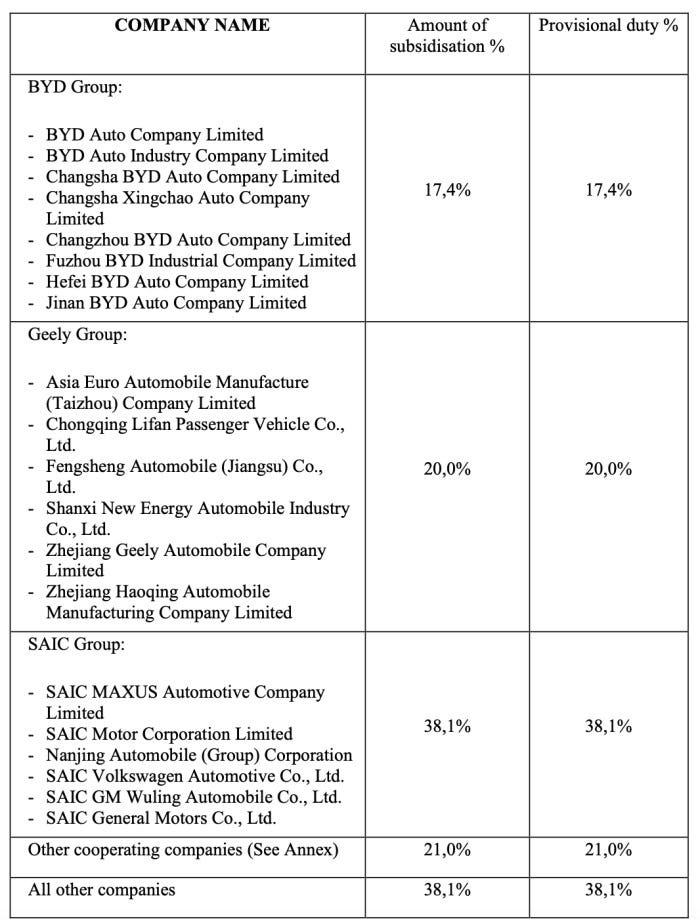

On Wednesday the European Commission announced it would provisionally apply the following tariffs to China-made electric vehicles, following the results of its anti-subsidy investigation:

I’m going to say I was a little bit right, in that the average tariff of 21 per cent for ‘all other cooperating companies’, and the tariffs applied to BYD (17.4 per cent) and Geely (20.0 per cent) is more or less in line with my central estimate of 10-20 per cent, and that I was right in saying that one of the companies would get whacked with a much higher duty.

But I wasn’t ambitious enough!

The 38.1 per cent for SAIC (which is in practice 48.1 per cent, 38.1+10), is rather high, and well above my 37.5 per cent all in upper estimate.

As I wrote in a snap reaction piece for FT Alphaville earlier this week, a few points to note:

The reporting on this story will be slightly confusing. These tariffs are in addition to the EU’s standard 10 per cent tariff on imported cars. So, the 21 per cent tariff, for example, on “other co-operating companies” amounts to a total tariff of 31 per cent (10 plus 21).

The range of tariffs applied to the sampled firms is perhaps indicative of either a wide range in degrees of state subsidisation (or at least evidence of state subsidisation), or a wide range in degrees of co-operation from the relevant companies. Or both. We won’t know for certain until the European Commission publishes more details.

These tariffs are highish, but not prohibitively high, at least for the two sampled firms with a lower rate and those in the “other co-operating companies” basket. My interpretation is that these are quite carefully calibrated to provide some additional protection to EU producers, while not antagonising China too much. I’ve written for Alphaville before about the possible retaliation risk, and we’ll find out soon enough whether the EU succeeds in avoiding a backlash from Beijing. In the EU’s favour: these tariffs are nowhere near the level of the US (102.5 per cent plus exclusion from IRA subsidies).

I expect that there will soon be news reports suggesting that China will bring a WTO challenge against these tariffs. From an EU perspective, this would be a good outcome. Both the EU and China are party to an arrangement called the MPIA, which essentially allows disputes to be seen through to conclusion despite the official WTO appeals function being borked. A worse outcome would be China retaliating outside of the confines of international trade law.

This isn’t the end of the story. Impacted companies now have some time to comment on the findings. The tariffs will then need to be made “definitive” by EU member states and have until the beginning of November to do so. This decision will be made via QMV. This means there is still time for member states to build a coalition in opposition to the tariffs, but it will be tricky. If definitively imposed, the tariffs usually last for five years.

These tariffs apply to imports from China. But lots of these firms also make, or are planning to make, vehicles elsewhere. This leads me to believe that, if these tariffs stick, there will be further discussions in the coming years about tariff circumvention and pressure to spread the tariff net further.

Building on the final point, what do companies exporting from China do now?

There are a few different options, none of which are mutually exclusive:

Sell somewhere else. The new EU tariffs could lead to Chinese companies, as they have done for the US, for the most part, giving up on the EU and exporting elsewhere. A recent piece by Global Trade Alert’s Angelo Krueger and Fernando Martin finds some evidence of this already happening:

According to Trade Data Monitor, 32% of global Chinese EVs exports ended up in the EU during Q1 2024. This is down from 42% in the comparable period in 2023. Over the same time frame Chinese EV exports to Brazil rose 4.5 percentage points. Kyrgyzstan and South Korea each saw ~3.5 percentage point rises. The rise in Chinese EV exports to these 3 markets during Q1 2024 was 2.6 times larger than the fall in Chinese EV exports to the EU.

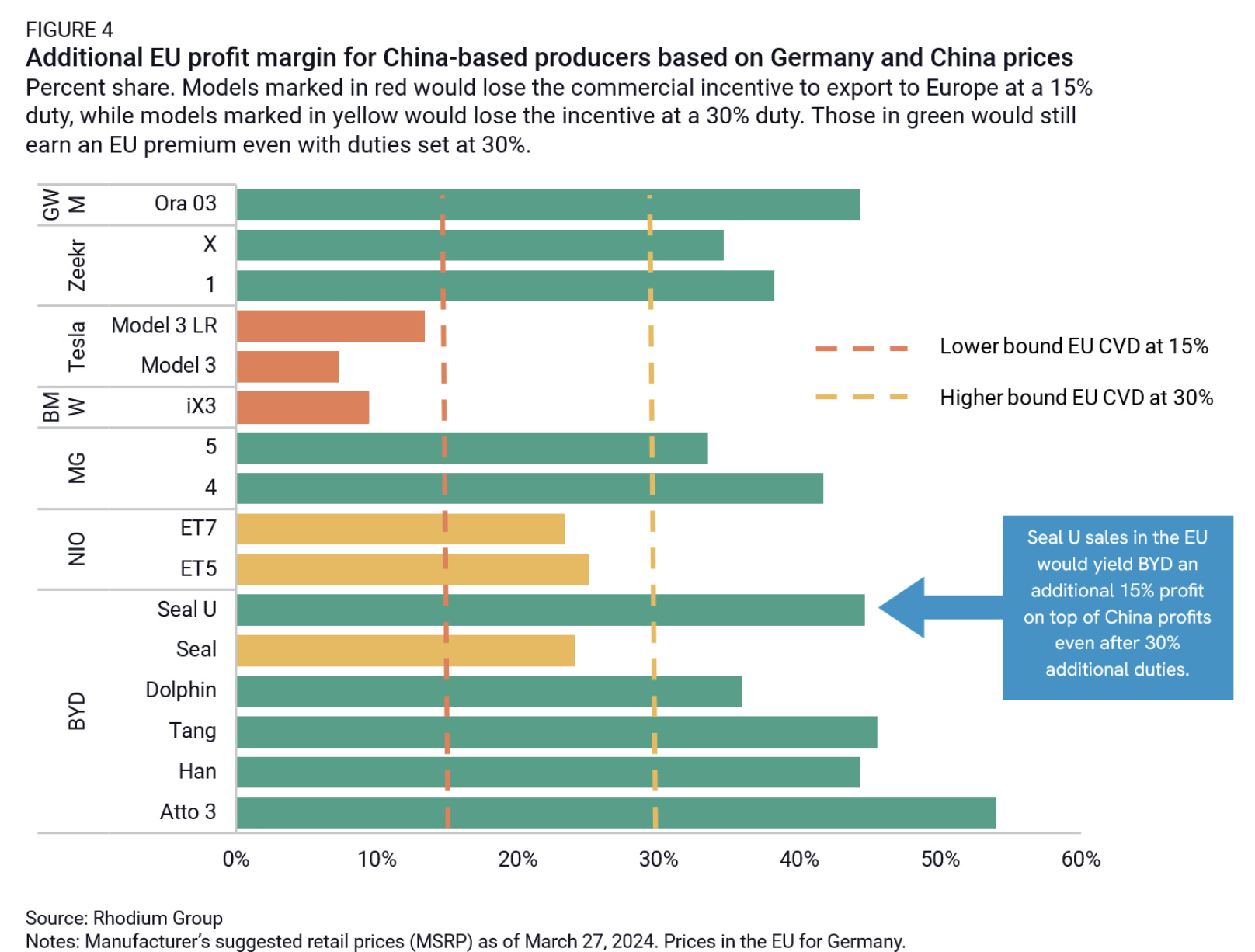

Absorb the tariff. Some China-based producers, particularly China-brand producers, are making bank when selling abroad. Research by the Rhodium group [see the chart below] finds that the EU tariffs won’t stop, for example, BYD making significant profits on their EU sales. This gives them significant scope to absorb the additional tariff costs, avoid passing them through to the end consumer, and retain a competitive price point in the EU.

Make the cars in the EU. One way to dodge tariffs is to make electric vehicles in-market, in this case, the EU. Some European policymakers are publicly advocating for this to happen — France’s economy minister, Bruno Le Maire, said “France welcomes all industrial projects. BYD and the Chinese auto industry are very welcome in France.” But this option isn’t necessarily straightforward, given the new EU foreign subsidies regulation [more below], and the possibility that the EU will investigate and penalise any EU-based Chinese auto-investment on the basis it is benefiting from … Chinese state subsidies.

Make the cars somewhere else and export them to the EU. There are two different versions of this. The first is more fraudulent: you still make most of the cars in China, but then ship them to Vietnam or the like, slap on a “made in Vietnam sticker”, and then export them to the EU. This is the sort of tariff circumvention that the Commission will be keeping an eye out for and, I would imagine, will crack down on pretty quickly — although doing so could end up resembling trade defence whack-a-mole. The second is more complex: Chinese firms are opening factories and production sites all over the world. It is perfectly plausible, for example, that a company decides to make cars in say, India or Saudi Arabia, and then export them to the EU. This would dodge the tariffs in the first instance, but could trigger another anti-subsidy trade investigation if the Commission suspects they are still unfairly benefiting from state subsidies (either Chinese or from the host state). This second outcome becomes particularly interesting if it involves exporting the cars to the EU from a country that has a free trade agreement with the EU … for example, the UK. [Ed: yes, I am stirring]

In practice, depending on the company, its international presence, the tariff level, etc, I think we will see a mixture of all of the above. Which means this story is far from over.

It’s not all about China

Overshadowed by all the EV talk, the Commission has opened a foreign subsidies regulation investigation into “the acquisition by the Emirates Telecommunications Group Company PJSC (‘e&') of sole control of PPF Telecom Group B.V. (‘PPF'), excluding its Czech business.”

Keep reading with a 7-day free trial

Subscribe to Most Favoured Nation to keep reading this post and get 7 days of free access to the full post archives.