Most Favoured Nation: The Berne Financial Services Agreement

UK-CH financial services trade, GINI and Tonic, Cost of Brexit and Customs Derrangement

Welcome to the 124th edition of Most Favoured Nation. The full post is for paid subscribers only, but you can sign up for a free trial below.

One of the more annoying phases of the early Brexit debate was when a load of people with very little prior knowledge about anything decided to tell people that there need be no UK-EU regulatory friction post-Brexit due to something called mutual recognition.

Mutual recognition, in this case, was presented as two countries agreeing to accept each other’s regulatory outcomes as being the same, even if the regulations and obligations themselves differed, removing the need to duplicate compliance procedures, for border checks and the like.

All the UK needed to do was convince the EU to accept mutual recognition — which is what every other country in the world uses — and all will be well.

The problem with this argument was that … well it’s not at all representative of reality. There are hardly any examples of comprehensive, mutual recognition between countries. Where it does exist, it is either in the context of much greater regulatory harmonisation (within the EU, or between Australia and New Zealand), or very narrowly applied (in the context of mutual recognition of conformity assessment, of professional qualifications, or of authorised economic operator programmes).

The limiting factor preventing the proliferation of mutual recognition is [a lack of] trust. One country needs to be able to trust that, despite the rules potentially being different, another country’s regulators and rules will ensure that nothing goes wrong, and if it does go wrong the culprits are appropriately punished. This is particularly true of highly regulated sectors.

All of this is a long-winded lead-up to saying the UK and Switzerland may have truly done something innovative with their new mutual recognition agreement for financial services, the so-called ‘Berne Financial Services Agreement’ (because it was signed in Berne, obviously).

For the reasons listed above, mutual recognition agreements in financial services are rare and where they do exist don’t work very well (see for example the 2008 US SEC-Australia MRA covering stock exchanges, which to my knowledge hasn’t ever actually been used). To facilitate cross-border activity, countries and regulators tend to prefer to rely on unilateral regimes such as equivalence, which can be withdrawn quickly if something goes wrong, or just approach it on a case-by-case basis.

The new UK-Swiss financial services deal goes a fair bit further, at least for the sectors covered: wholesale and high-net-worth individuals (HNWI).

Regulatory cooperation

At the institutional level, this means a new architecture with rules around the withdrawal of market access, dispute settlement and regulatory cooperation. For at least some of the market access commitments (those based on the principle of deference, which recognises the other’s regulatory outcomes as equivalent even if the requirements are different) withdrawal of benefits would no longer be near-instantaneous, as is the case with equivalence, and there would instead be a 6 month period in which all parties would try and work out another solution.

Market Access

My general test for whether an agreement actually delivers new market access for foreign services firms — which pretty much every free trade agreement fails — is whether it requires a country to change its domestic regulation as a result.

In this instance … the agreement seems like it will indeed require that to happen across three areas: insurance; investment services provided to UK HNWIs; and UK investment services provided to Swiss sophisticated investors:

Insurance. The UK will be the sole trading partner exempted from new Swiss legislation which will require overseas insurance brokers to localise in Switzerland from 2024. Once implemented UK insurance firms will be able to provide insurance policies in the space of renewable energy, directors’ & officers’ liability, sellers and buyers warranty, indemnity, and cyber insurance. Life insurance, accident & health insurance, monopoly and business interruption insurance are still excluded; liability insurance is only for specific professional policyholders.

Investment services provided to UK HNWIs. Apparently this is based on existing UK legislation related to something called MIFIR 47, which was folded into the UK Financial Services Act 2023, but goes further. Swiss investment services providers will be able to access a more simplified, streamlined procedure when doing business with UK HNWIs. Also, it leaves open the option of firms relying on the Overseas Person Exclusion (OPE). (I am informed that a previous quirk of MIFIR 47 was that if it was turned on the OPE route was turned off, so this tweak is an improvement.)

UK investment services provided to Swiss sophisticated investors. The Swiss are going to change some rules meaning “Client advisers will no longer need to be registered by Swiss registration bodies, nor will they have to prove to these bodies that they meet the requirements necessary to provide their services to private clients in Switzerland. This will do away with the need to sit examinations and provide documentation relevant to the registration process."

Anyhow, this all looks pretty innovative. It also leaves me slightly confused as to why the UK pushed this out quietly in a press release just before Christmas and otherwise barely mentioned it all. Slightly odd given the propensity to hype things that aren’t as impressive, but well done anyway!

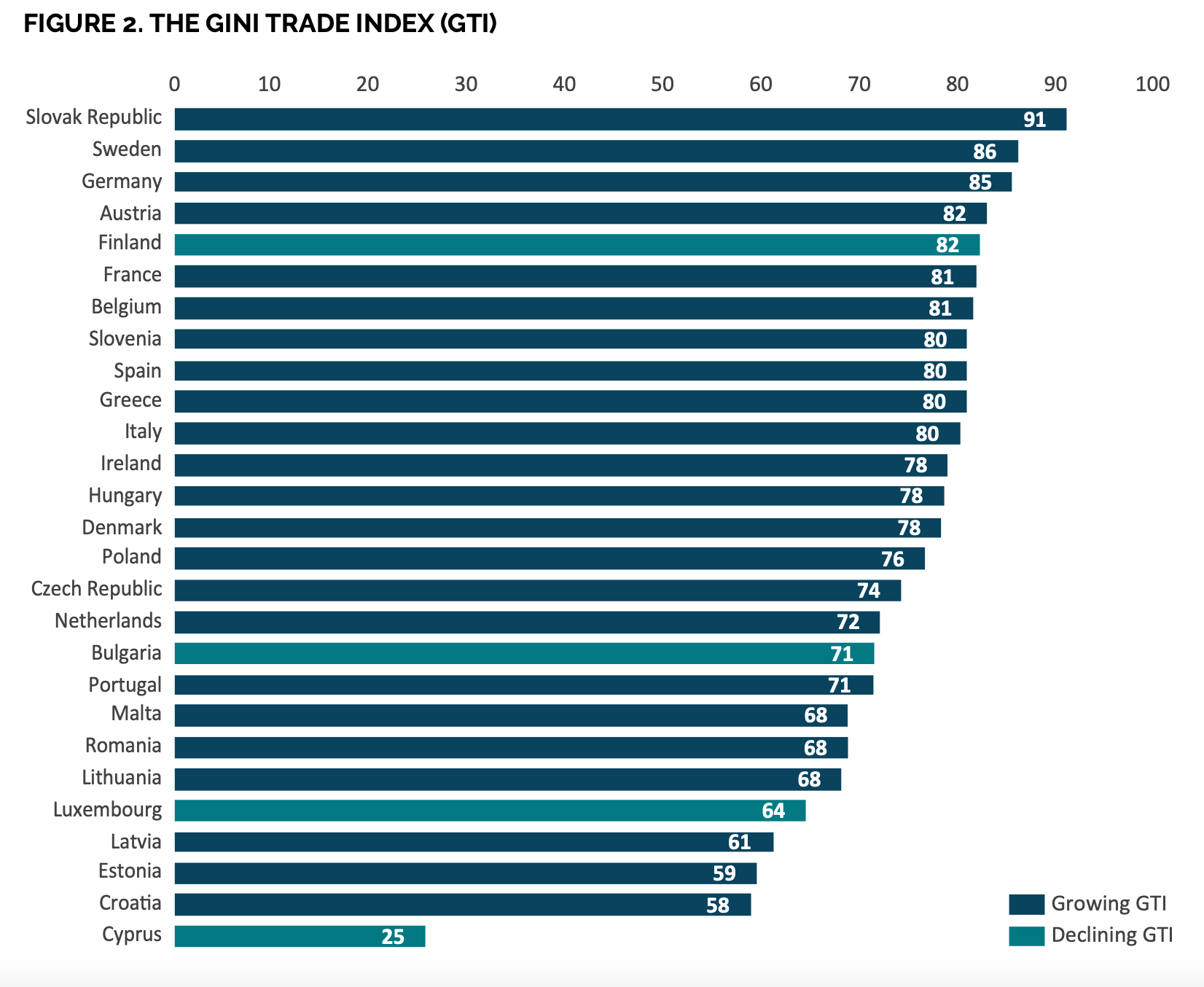

GINI and Tonic

DG Trade’s procurement Tsar, Lucian Cernat, has published a new paper for ECIPE proposing a new measure of trade equity: The GINI Trade Index. Based on the GINI Coefficent — a measure of a income inequality within a country — the GINI trade Index is an indicator of firm-level trade participation in a country’s exports. A score of 100 would mean that there is only one exporter responsible for the entire export value of the country. A country where all exporters would export equal values would have a score of zero.

Keep reading with a 7-day free trial

Subscribe to Most Favoured Nation to keep reading this post and get 7 days of free access to the full post archives.