Performative Policy Making

Tariffs, disruption, rules of origin and Art Laffer

As has been widely reported, earlier this week the US decided to increase tariffs on several China-originating products.

You can see the full list here, with a note that many of these products have an additional MFN tariff applied as well (for example, for electric vehicles the new tariff is 100% plus the 2.5% MFN tariff).

Why has the US done this? Well, it kinda depends on who you ask. Earlier this week Dmitry Grozoubinski kindly wrote a guest piece for MFN exploring the various motivations, which you can read here.

My view: these tariffs are largely performative and, with some exceptions, will probably have little impact over and above the restrictions already in place. Where the new tariffs do create issues — as we have seen happen with the discriminatory conditions placed on IRA subsidies – the US will probably grant quiet exemptions and derogations to avoid supply chains falling over completely.

Take electric vehicles — the existing 27.5% tariff and exclusion from IRA consumer subsidies already means that the US isn’t importing much in the way of Chinese electric vehicles. See the yellow line right at the bottom of the chart:

Anyhow, here are some additional thoughts in no particular order:

This decision by the US potentially makes it easier for the EU to introduce its own, more proportionate, tariff on Chinese EVs. The EU’s antisubsidy investigation into Chinese EVs will conclude soon, and European industry is starting to get a bit antsy, fearing Chinese retaliation. Assuming the EU tariffs are in the range of 10-20%, on top of the existing 10%, and have a fairly solid evidence base to support them, DG Trade could possibly get away with saying “Hey, we just did some tariffs following the normal legal route, don’t get mad at us [subtext: it could have been worse **points at the US**]”.

On a similar note, the EU could also use the US tariff hike as an excuse to push its own tariff higher, if not anywhere near as high as the US. There is already a reasonable chance that the China-brand firms that have been included in DG Trade’s sample for its investigation will face higher tariffs than everyone else due to their alleged non-cooperation, but the US’s 102.5% tariff might provide a bit of extra cover. Saying that, the EU still won’t want to go too hard because it will probably have to face down a WTO challenge from China. I know what you’re thinking, the WTO dispute settlement process if broken etc etc … but people forget that both the EU and China have signed up to the MPIA, meaning a dispute could be seen through to conclusion.

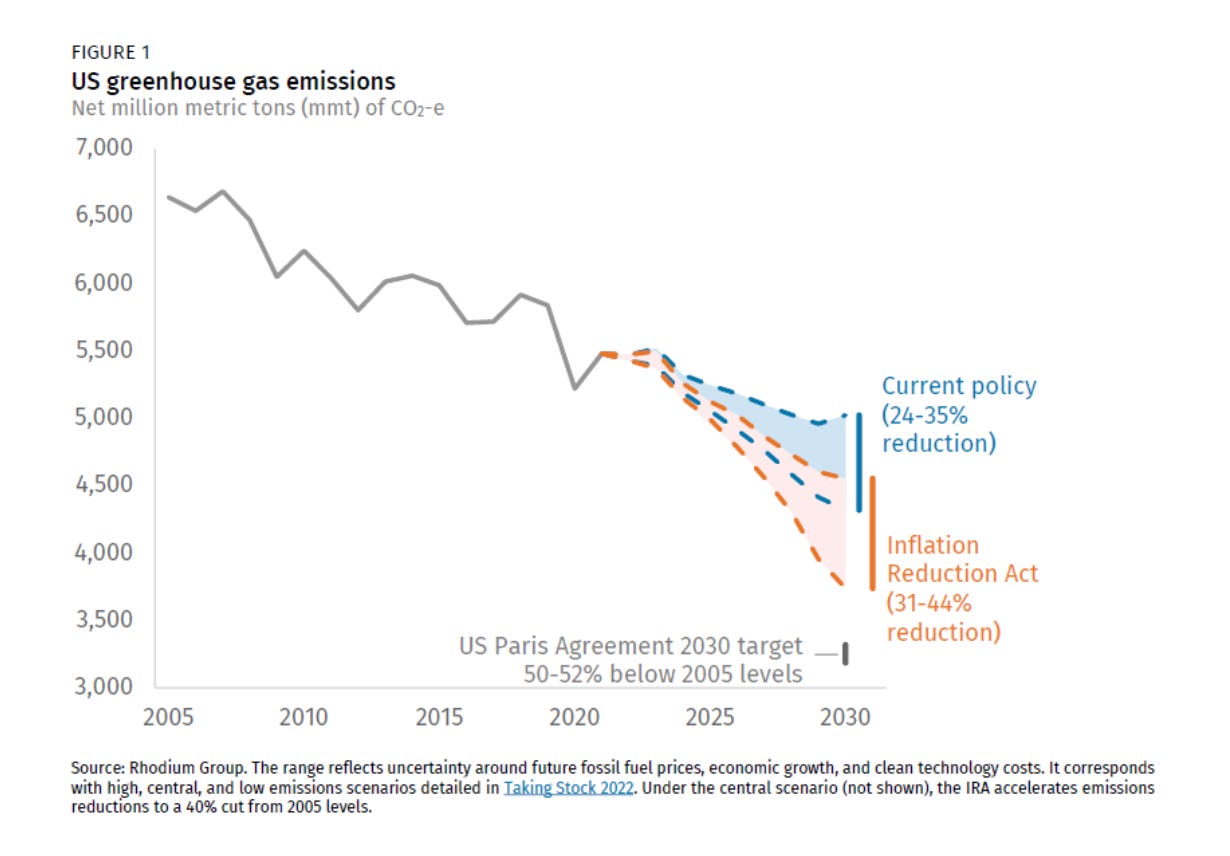

As readers of this newsletter might know, I’m not fully convinced by the environmental rationale for any of these actions. To the rest of the world, tariffs such as these on green goods, as well as others on steel and aluminium, are primarily designed to win votes from specific US voting segments — any second-order environmental benefit is a bonus and not always obvious. I had a look at the climate benefits of the Inflation Reduction Act and it seems to net out just about positive, but there’s not much in it:

Anyhow, the main argument you see is that Americans won’t support the green transition unless it also results in jobs. I mean, I kinda get that. But to my mind, the more honest argument is “Protectionism will ensure Biden gets elected and Biden will do more to tackle climate change than Trump.” Which, if it works, sure, but please stop asking people to believe the other stuff.

Disruption in the Red Sea?

Some new research has found that the attacks by Houthi Rebels in the Red Sea have so far had only a small negative impact on global trade and inflation.

The authors argue that:

The economic effects are likely attenuated by current conditions characterised by spare capacity in global shipping, little port congestion, subdued global demand, and the adequate stock of inventories.

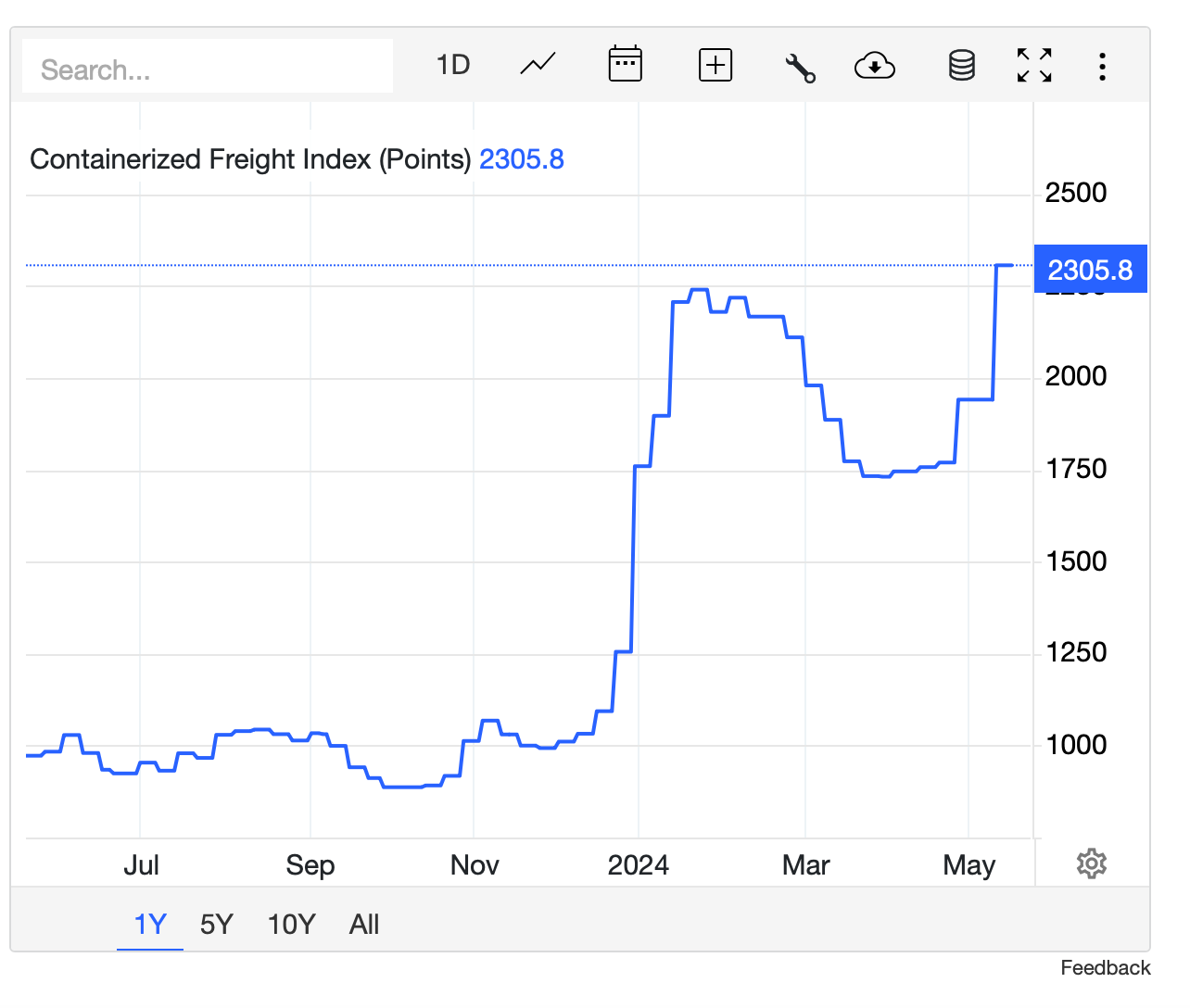

This sounds about right, and it brings me to one of my favourite topics: choosing the correct start date for charts.

By which I mean, both of these charts are factually correct, but tell a very different story about the impact of recent events on the cost of freight in the grand scheme of things:

Chart 1

Chart 2

Or, if you prefer your information in meme form:

Factoid of the week

From Bryan Riley on Twitter:

Chart of the week

From a recent report by the Atlantic Council:

Art Laffer, but for rules of origin

With thanks to Dan Ciurak for flagging, a new research paper applies the theory of Art Laffer to rules of origin.

For those of you unfamiliar, Laffer’s theory is that once a government raises tax levels beyond a certain point it actually leads to a reduction in tax revenues due to people becoming more incentivised to find ways to avoid paying, moving to other countries, etc.

It looks something like this:

In reality, this is one of those observations that has some merit, but in policy-making terms is much abused because people who hate tax always miraculously seem to conclude a country is on the right-hand side of the curve and, if they engage with it at all, those who love tax on the left-hand side.

Anyhow, back to rules of origin.

In summary, strict rules of origin requirements are found to incentivise local sourcing — so as to allow the exports of firms to qualify for the preferential tariffs on the relevant free trade agreement – but only to a point. If the requirements are too arduous, firms eventually just decide to suck up the tariff and give up on regional sourcing.

The impact also depends slightly on the ability of firms to relocate production facilities.

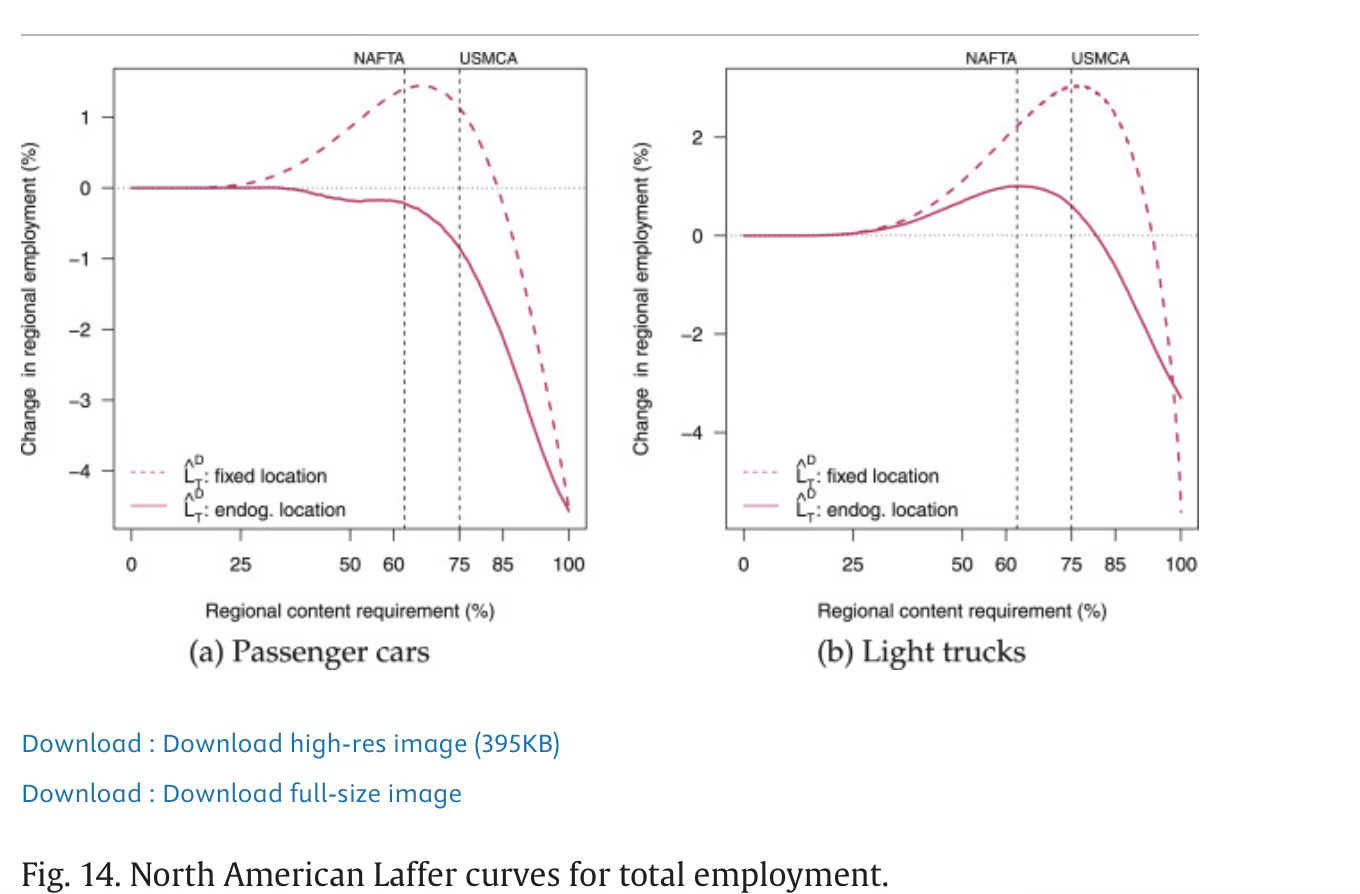

The authors look at the impact of the stricter requirements of USMCA (vs NAFTA) on US/Can/Mexico trade and find:

The effects of the 75% RoO imposed in 2020 depend on the relevant tariff and the ability to relocate assembly. With fixed assembly locations, the higher RoO reduces employment in all three countries for cars, where tariffs are low. For trucks, the 25% US tariff induces more compliance in Canada and Mexico, increasing employment in those countries. With the option to relocate assembly, higher RoOs redistribute employment to the US, but Canada and Mexico lose more, leading to a half percent decline in North American employment for both cars and trucks.

And the RoO Laffer curve ends up looking like this:

Best wishes,

Sam