I am on holiday.

Last Friday (23 May), just before my flight took off, President Trump announced he was going to hit the EU with a 50 per cent tariff on 1 June because he did not like the cut of its jib. [Side note: thank you to the other people on Flint’s excellent trade team for ensuring this outburst did not, in fact, ruin said holiday.]

On Sunday (25 May), Trump had a chat with European Commission President Ursula von der Leyen and agreed to delay the 50 per cent tariff until 9 July to allow more time for negotiation.

This has led to much amusement on Bluesky and other social media platforms. He bottled it, again.

Some have, in fact, observed a repeat pattern of Trump making threats and then bottling it.

The Financial Times’ Rob Armstrong has even coined a term for it: TACO. Trump Always Chickens Out.

Buuuuuuut, does he actually?

First, yeah, he tends to chicken out of his absolutely insane threats. Not always straight away. But eventually. [Also, if you’re gambling speculating on international markets, which is the thing Rob writes about (TACO was invented in the context of the “TACO trade”), then listen to Rob and ignore me.]

But I also find myself thinking Trump does a pretty good job of re-defining what is “normal”.

To put it another way …

Sure, he announced a pause of the country-specific reciprocal tariffs (e.g. 20 per cent on the EU, 46 per cent on Vietnam, 26 per cent on Thailand, etc.), but he still hit everyone with an additional 10 per cent tariff.

Sure, he has backed away from the 125 per cent tariff on China, but he’s still upped the applied tariff level by at least 30 per cent (10 per cent baseline tariff + 20 per cent reciprocal tariff), in most instances and killed the trade B to C parcels.

Sure, he has backed off on quite a few things, but he has still imposed a 25 per cent tariff on imported automobiles, parts, steel, and aluminium. (There will probably be more to come on pharmaceuticals, for example.)

Sure, he softened the blow of some of the aforementioned tariffs on automobiles imported from Mexico and Canada by excluding the US-originating value of cars that qualify for USMCA, but qualifying for this exemption is fiendishly complicated.

Here’s a useful chart by the New York Times (h/t Deborah Elms).

You get the point.

Anyway, at the end of the Presidency, I expect the aggregate applied US tariff to be 10-20 percentage points higher than it was at the beginning. Within this average, I expect there to be some pretty significant country and product-specific variation. The US will be significantly more closed to international trade than it was one day one. All of which kinda matters, I think.

And that’s because, well, Trump Does Not Always Actually Chicken Out. Or T[dn]A[a]CO. Even if it feels like he does.

Chart of the week

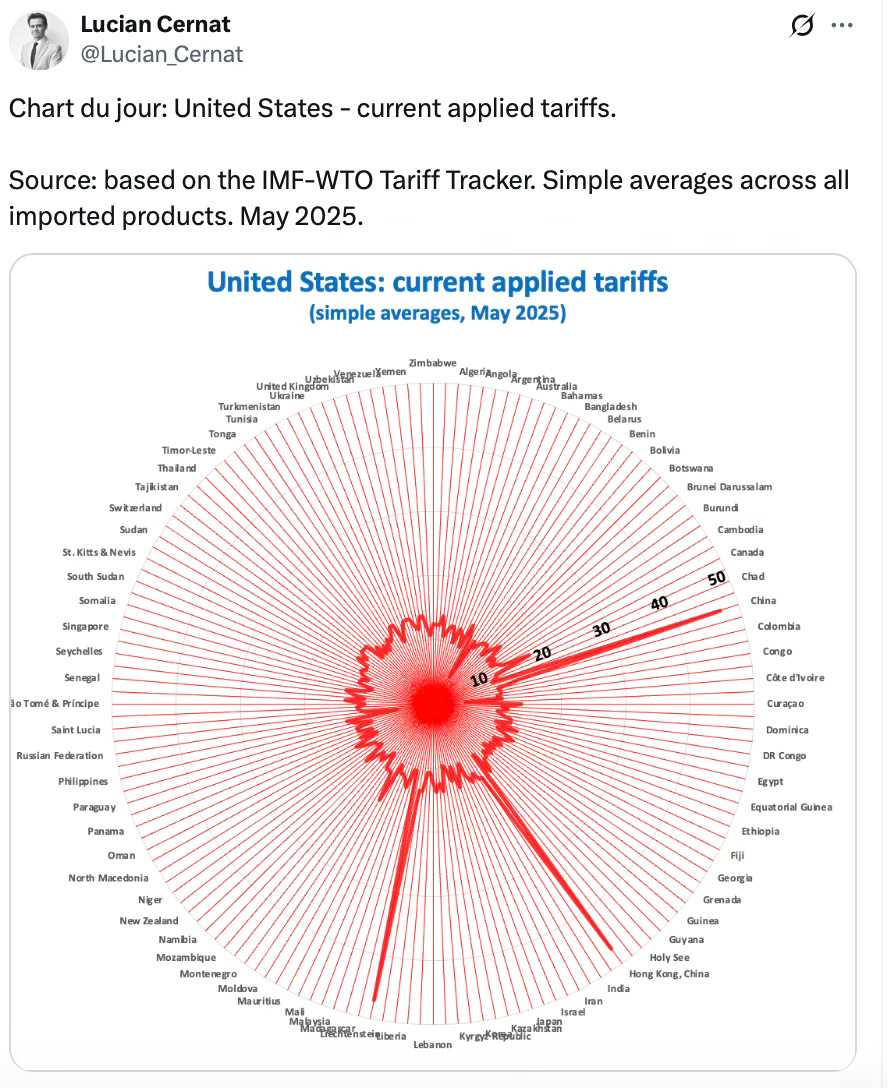

Following on from the discussion above, here’s a chart by Lucian Cernat visualising the current applied US tariff (note: I’m guessing the big spike at 35ish minute mark is Macau):

Something different

My colleague James Crabtree, of writing a very good book about India fame, sent me this Peter Frankopan Substack piece about Venetian beads.

Why?

Well, because the beads turned up in Alaska before Colombus showed up. And they likely got there via Eurasian trade routes.

Check it out.

Holiday snap

With my youngest research assistant.

Best,

Sam

Seeing that chart really highlights how big the tariff differential is. How big a problem/market is laundering countries of origin going to be? Like it seems pretty plausible and profitable to send a truck full of widgets over the border from China to Vietnam where they can come fresh out of a "factory".

https://substack.com/@hoffmania/note/c-121938107?r=4ptpw5&utm_medium=ios&utm_source=notes-share-action