Tariffs and the national interest

How to choose and some predictions

Happy New Year!

In the context of the upcoming Trump trade wars, I have been thinking about the concept of the National Interest [very serious voice]. In particular, on what basis do countries decide whether to cave to Trump’s demands or face down the penalty tariffs?

In particular, assuming one of Trump’s demands is that US allies follow his lead on applying tariffs to China, how do countries decide whether that is a good idea?

There is probably a really clever way to do this. You could create a model that considers trade, national security interests, economic security interests, investment needs, industrial strategy, etc., and make a thoughtful determination about how best to proceed.

There is also a much more reductive way, which doesn’t take into account the politics, national security dimension or any other important thing and instead focuses only on trade exposure.

For the purpose of this newsletter, I’m going to do the latter. (Obv.)

To work this out, I have done the following:

For both the EU and the UK, I used Google to find the 2023 dollar figures for exports to the US, imports from the US, exports to China, and imports from China.

I have assumed a consistent (as in, it applies to all exports and imports) trade elasticity of 0.8. In English, this means that I have assumed that a 1 per cent tariff increase leads to a 0.8 per cent reduction in trade. I have made this up, and it isn’t based on any literature; I just think that the standard elasticities, e.g. 2.156, are too high, so I’ve used vibes to conjure up a lower one. If you were doing this properly, you would probably want to use a different elasticity for the different countries involved and directions of trade. But I’m not.

I have created five tariff scenarios (see below) and applied them to trade between the UK/EU, the US, and China. Based on these scenarios, I have calculated the impact of different tariff configurations on total trade between tthese countries.

Before we get going, I would like to reiterate (again) that this is all very reductive and in no way should be mistaken for serious analysis. (For that, you need to pay me/my employer real money.)

Scenarios

The scenarios (above) are hopefully pretty self-explanatory, but in case it helps to see them written out:

Scenario one. Baseline scenario; no additional tariffs.

Scenario two. No additional tariffs on US trade; a very large (60%) UK/EU tariff on China and retaliatory Chinese tariffs of 5%.

Scenario three. No additional tariffs on US trade; a moderate (20%) UK/EU tariff on China and retaliatory Chinese tariffs of 5%.

Scenario four. A 10% US tariff on UK/EU exports and a retaliatory UK/EU tariff of 5%. No additional tariffs on China trade.

Scenario five. A 20% US tariff on UK/EU exports and a retaliatory UK/EU tariff of 7%. No additional tariffs on China trade.

In summary, Scenarios two and three look at a situation in which Trump convinces the UK/EU to apply new tariffs to China in return for being exempt from US tariffs; scenarios four and five look at a situation in which the UK/EU face Trump down and are hit with US tariffs.

Impact

As you would imagine, the impact of these scenarios is slightly different for the UK and the EU.

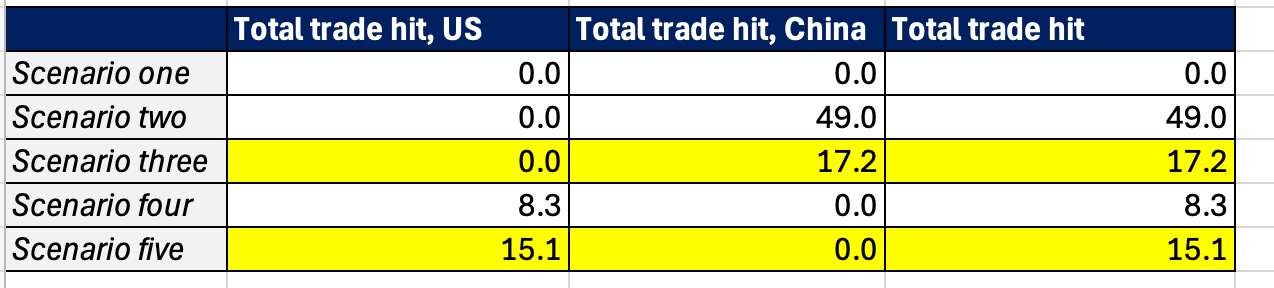

Starting with the UK:

Scenario two, in which Trump convinces the UK to apply a massive tariff to Chinese imports, creates the biggest impact, leading to a $49 billion hit to trade between the three.

However, scenario three — No additional tariffs on US trade; a moderate (20%) UK/EU tariff on China and retaliatory Chinese tariffs of 5% — and scenario five — A 20% US tariff on UK/EU exports and a retaliatory UK/EU tariff of 7%. No additional tariffs on China trade — throw out broadly similar numbers (highlighted).

In summary, according to my very crude assessment of the UK’s national interest, the UK would be absolutely mental to agree to any Trump proposal that involved applying tariffs of around 60 per cent to Chinese imports.

Equally, a ten percent tariff threat by the US (Scenario four) is probably too low to convince the UK to take an action on China.

However, if the US threatened a 20 per cent tariff (Scenario five) on UK exports unless the UK applied a 20 per cent tariff (Scenario three) to Chinese imports, the UK would be in a much tricker position, with the trade impact of either scenario broadly comparable.

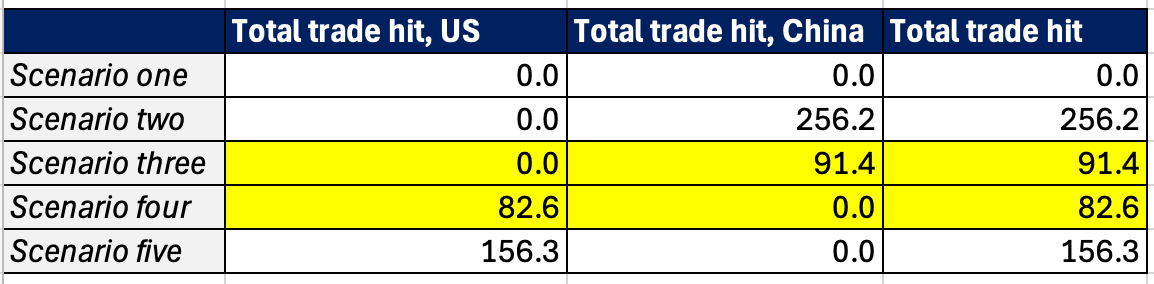

For the EU, the trade-offs are slightly different:

Here, Scenario two (massive tariffs on China) creates the biggest hit to total trade between the three, but Scenario five (a 20 per cent US tariff) is nothing to sniff at either.

More interesting is the similar impact of Scenario three (a 20 per cent tariff on China) and Scenario four (a 10 per cent US tariff) on total trade — at $91.4bn and $82.6 billion respectively. (Highlighted)

This suggests that if the US threatened a 10 per cent tariff (Scenario four) on EU exports unless the EU applied a 20 per cent tariff (Scenario three) to Chinese imports, the EU would have a serious decision to take.

Given the politics of China, the US may even be able to threaten higher tariffs (Scenario five) and push the EU into considering higher China tariffs (Scenario two).

On a comparative basis, this suggests that both

a) the UK and EU interests vis-a-vis the US and China are not directly aligned; and

b) caving to Trump threats only starts to be in the UK interest under very specific conditions (high US tariff threat/moderate tariff on China concession), wheras the EU faces a more difficult choice under all scenarios.

Fun!

I know everyone is doing there big lists about big things that will happen in 2025. In keeping with that, here are two slightly more specific things that I think will happen in 2025.

The EU will initiate a trade defence investigation into Chinese batteries

I’m not sure why I chose this one because I’m not particularly confident that this will happen in 2025. I am fairly confident, however, that this will happen at some point and that it could happen any time from now.

“Why?”, I hear you ask. Well, the writing has been on the wall for this one for a while. The EU has long had a strategic objective to develop onshore battery-making capabilities which has influenced the design of numerous bits of policy.

For example, the EU’s battery recycling regulation’s recycling and collection obligations and carbon footprint obligations are both designed to encourage local production. Then there’s the EU-UK Trade and Cooperation Agreement, which from 2027 will only allow electric vehicles to be trade tariff-free if the batteries originate in either the EU or the UK.

I wrote about this for FT Alphaville at the time, but the main reason I think this is coming soon is that the EU’s anti-subsidy investigation into Chinese electric vehicles spent a lot of time and energy arguing that the Chinese battery industry should be treated as a heavily subsidised state-owned industry.

So yeah, EU battery tariffs.

UK will introduce new rules on forced labour in supply chains

The UK is a bit of an outlier compared to the US and EU on dealing with forced labour in supply chains. The US has its Withhold Release Orders and Uyghur Forced Labor Prevention Act and the EU has its Corporate Sustainability Due Dilligence Directive (CSDDD) and forced labour regulation.

As well as general FOMO, the UK has come under some pressure to introduce its owns rules from, for example, the US in the context of its negoitations for a critical minerals deal.

There has also been a fair bit of domestic pressure from prominent MPs in both the Conservative and Labour party, with a particular focus on solar panels coming from China.

Anyhow, it looks like the UK government is going to do something about this.

In the context of updating existing Modern Slavery rules, the UK goverment said [emphasis added]:

The government is reviewing how it can strengthen penalties for non-compliance and create a proportionate enforcement regime. However, this will require legislative change and will need to be considered against a wider review of how best the government can use legislative and non-legislative measures to tackle forced labour and increase transparency in global supply chains. The government will set out next steps more broadly in due course.

So yeah, seems likely we’re going to see something on this.

Best wishes,

Sam

Fun piece! I’d argue however that the much bigger issue on UK-US relations is the possibility of a hefty services trade deal between the two. There’s little reason why Trump should oppose this, and should it be big enough to provide a substantial boost then combined with the advantages of de-risking, it may make Chinese tariffs a good deal easier to swallow.